WengYang Industrial Zone Yueqing Wenzhou 325000

Work Hours

Monday to Friday: 7AM - 7PM

Weekend: 10AM - 5PM

WengYang Industrial Zone Yueqing Wenzhou 325000

Work Hours

Monday to Friday: 7AM - 7PM

Weekend: 10AM - 5PM

The years 2025 and 2026 will be remembered as a period of unprecedented turbulence for the global solar industry. An economic supercycle, driven by the global energy transition and digital transformation, triggered a historic surge in the prices of copper and silver—two metals fundamental to the safety, reliability, and efficiency of photovoltaic (PV) systems. This commodity crisis sent shockwaves through the supply chain, squeezing margins, challenging production norms, and threatening the pace of solar adoption worldwide. For manufacturers of critical PV electrical components, it was a moment of truth.

At cnkuangya.com, this challenge was not a threat but a catalyst. It was an event that we had anticipated through rigorous market intelligence and one that we met with a clear, decisive strategy. While others scrambled to react, we executed a prepared, three-pillar response built on Proactive Procurement, Process Optimization, and Transparent Partnership. This approach allowed us to navigate the storm, not by cutting corners or compromising on quality, but by doubling down on our core values of engineering excellence and customer commitment. The result? We emerged from the crisis not just intact, but stronger, more innovative, and more resilient than ever, with a reinforced market position and a product portfolio forged in the fires of adversity. This is the story of how we turned the greatest market challenge in a decade into our greatest opportunity for leadership.

The lead-up to 2025 was marked by a convergence of powerful global forces. As the world accelerated its push toward decarbonization, demand for renewable energy technologies and electric vehicles (EVs) soared. Simultaneously, the rapid expansion of artificial intelligence and data center infrastructure created a voracious appetite for high-conductivity metals. This demand surge collided head-on with a landscape of constrained supply, geopolitical friction, and macroeconomic uncertainty, creating the perfect storm for a commodity supercycle. At cnkuangya.com, we tracked these trends with intense focus, recognizing that the stability of our industry was intrinsically linked to the volatile markets for copper and silver.

Copper, the backbone of the electrical world, experienced a meteoric rise. Driven by its critical role in EVs, which use up to four times more copper than conventional cars, and massive grid expansion projects, demand fundamentally outstripped supply. Mining disruptions in key producing regions and U.S. trade policies, including a 50% tariff on certain copper products, further tightened the market. Prices climbed relentlessly throughout 2025, with benchmark prices surging by over 36% to hit levels not seen since 2009, peaking at over $5.50 per pound (approaching $12,000 per metric ton) by the year’s end 1. For an industry reliant on copper for everything from wiring and busbars to internal componentry, this was a direct and significant threat to cost structures.

The story for silver was even more dramatic. Playing a dual role as a safe-haven investment and an indispensable industrial material, silver was caught in a “perfect squeeze.” As investors flocked to precious metals amidst a weakening U.S. dollar and inflation fears, industrial demand—led by the PV industry itself—exploded. The conductive silver paste used in solar cell manufacturing became a primary driver of this demand. The result was a staggering price surge of over 140% in 2025, with prices briefly topping $72 per ounce before peaking near $84 per ounce in some markets by December . For some solar module manufacturers, silver’s contribution to total production cost ballooned from a manageable 5% to a staggering 17% . This volatility threatened to derail the cost-reduction roadmap that had defined the solar industry for over a decade.

[EMBED: Timeline diagram showing silver price trends from Q1 2025 - Q4 2026]

These twin crises were not short-term fluctuations; they represented a structural shift in the global economy. At Kuangya, we understood that navigating this new reality required more than just temporary fixes. It demanded a fundamental re-evaluation of our products, processes, and partnerships.

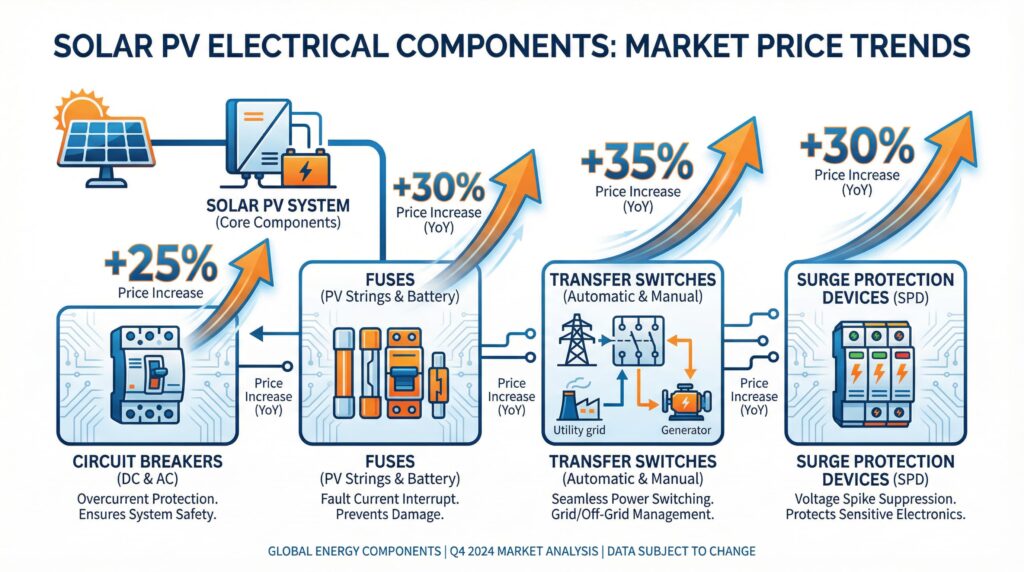

Electrical balance-of-system (BOS) components, while often overlooked in favor of the solar module, are the guardians of a PV system’s safety, longevity, and efficiency. They are the circuit breakers that prevent catastrophic failures, the fuses that protect sensitive equipment, and the switches that ensure uninterrupted power. The integrity of these components is non-negotiable. However, their construction is deeply reliant on copper and, in some specialized cases, silver. The 2025-2026 price surge therefore translated directly into intense manufacturing challenges, forcing a painful choice between absorbing unsustainable costs, raising prices, or—for less scrupulous manufacturers—compromising on material quality.

At Kuangya, the third option was never on the table. Instead, we undertook a rigorous analysis of the cost impact across our core product lines to inform our engineering and procurement strategies.

The following table summarizes the acute impact of the commodity crisis on our key product categories, revealing how rising metal costs created distinct manufacturing and design challenges for each.

| Component | Key Materials | Avg. Cost Impact (Pre-2025) | Peak Cost Impact (Q3 2025) | Resulting Mfg. Challenge |

|---|---|---|---|---|

| DC/AC Circuit Breakers (MCB) | Copper | Low | +40% | Balancing thermal performance and conductivity with smaller, more expensive copper parts. |

| gPV Fuses | Silver, Copper | Medium | +65% | Maintaining precise interrupting ratings and low power loss without using cheaper, less reliable materials. |

| Automatic Transfer Switches (ATS) | Copper | High | +50% | Redesigning high-current busbars and terminals to manage immense thermal loads under extreme cost constraints. |

| Surge Protection Devices (SPD) | Copper, Zinc Oxide | Low | +35% | Ensuring microsecond response times and device longevity when the cost of internal copper conductors skyrocketed. |

DC/AC Circuit Breakers (MCBs): The heart of an MCB is its bimetallic strip and magnetic coil, both of which rely on high-purity copper for their conductive and thermal properties. The 40% surge in copper-related costs directly affected the trip mechanism that distinguishes a safe overload from a dangerous short circuit. The challenge became one of engineering precision: how to maintain the exact thermal expansion and conductivity characteristics required for reliable tripping while battling unprecedented cost pressures. Any substitution with lower-grade alloys would risk delayed response times, fundamentally compromising the device’s safety function.

gPV Fuses: Specialized gPV fuses, designed for the unique demands of solar circuits, depend on a precisely engineered fuse element. This element, often made of pure silver or a silver-plated copper alloy, is designed to melt at a specific current and voltage to protect downstream equipment. With silver prices soaring and fuse element costs jumping by up to 65%, the temptation to use less precise, cheaper materials was immense. For us, this was a red line. Maintaining the TUV and UL-certified interrupting rating and energy let-through (I²t) values was paramount. The crisis forced us to focus on manufacturing innovations that reduced waste in the stamping and plating of these critical elements, rather than altering the core material itself.

Automatic Transfer Switches (ATS): An ATS is a high-current device by nature. Its internal busbars, contacts, and lugs are substantial pieces of copper, designed to carry heavy electrical loads with minimal heat generation. As copper costs climbed by 50% for these components, the primary engineering challenge became thermal management. Simply reducing the amount of copper to save costs would lead to higher resistance, generating more heat and creating a significant fire hazard. Our R&D teams had to pioneer new busbar geometries and connection technologies to maintain safe operating temperatures while optimizing material usage to the gram.

Surge Protection Devices (SPDs): While the copper content in an SPD is lower than in an ATS, it is no less critical. The internal conductors that divert surge currents to ground must have extremely low impedance to react in nanoseconds. The 35% cost increase in these copper components put pressure on the very heart of the SPD’s function. The manufacturing challenge here was to preserve the high-speed protective pathway without compromise, ensuring the device could handle repeated surge events over its lifespan, a commitment we upheld through stringent quality control and design validation.

Across the board, the commodity crisis was a direct assault on the quality and integrity of PV electrical components. Our response had to be equally direct and rooted in a deep commitment to engineering first principles.

In the face of market-wide panic, our strategy at Kuangya was guided by a single principle: control what we can control. We could not influence global commodity prices, but we could master our supply chain, optimize our operations, and deepen our partnerships. We activated a multi-faceted plan centered on three pillars, designed not just to survive the crisis but to build a more robust and agile company.

Long before the market peaks of late 2025, our sourcing teams had identified the risk of a commodity squeeze. We acted decisively, shifting from short-term purchasing to a long-term, strategic sourcing model.

With material costs soaring, every gram of waste mattered. We launched an aggressive internal campaign to enhance production efficiency, framed not as a cost-cutting measure, but as a quality-enhancement initiative.

We believe that true partners communicate openly, especially during difficult times. While competitors implemented sudden, drastic price hikes or went silent, we chose a path of radical transparency.

Critically, during this period of intense cost pressure, we made a counter-intuitive strategic decision: we doubled down on our commitment to global certifications. In 2025, as some in the market were tempted to substitute materials, we successfully secured new and updated UL, TUV, and CE certifications for our core product lines. This was a powerful, tangible statement to the market. It demonstrated that our commitment to safety and quality was absolute and non-negotiable, regardless of market conditions. This act of leadership not only justified our value proposition but also provided our customers with the ultimate assurance: with Kuangya, the standards are never compromised.

[EMBED: Generated image celebrating "Certification Excellence" with logos of certification bodies and a statement of quality]

Market crises are powerful catalysts for innovation. The 2025-2026 commodity surge was no exception. For our Research & Development team at Kuangya, it was a call to action—a mandate to engineer our way out of the crisis by fundamentally rethinking material science and product design. The pressure to reduce our reliance on volatile commodities did not lead to compromises; it led to breakthroughs that have made our products more efficient, robust, and cost-effective for the long term.

Our first line of attack was the metals themselves. We initiated a fast-tracked research program aimed at reducing our dependency on pure copper and silver without sacrificing performance.

The crisis forced our product designers to embrace a philosophy of “intelligent minimalism.” The goal was to achieve maximum performance with minimal material.

These R&D achievements would not have been possible at the required speed without our deep investment in digitalization. We leveraged digital twinning and advanced simulation software to create virtual prototypes of our new designs. This allowed us to run hundreds of thermal, electrical, and mechanical stress tests in a simulated environment, rapidly iterating on designs without the time and expense of building physical prototypes for each version. This digital-first approach cut our development cycle for the new ATS busbar from a projected nine months down to just four, enabling us to bring a more cost-effective solution to market when our customers needed it most.

The turbulence of 2025-2026 has passed, but it has left behind a changed landscape. A “new normal” for commodity prices has been established, and the industry now understands that supply chain resilience is as important as product performance. At cnkuangya.com, we do not see this as an obstacle. We see it as the foundation for the next wave of innovation. Having navigated the crisis, we have emerged stronger, more agile, and with a clear vision for the future.

We are proud to unveil our development focus for the coming year, a roadmap designed to address the evolving needs of the global solar market:

The 2025-2026 commodity crisis was a defining test for our industry and our company. It was a trial by fire that forged our strategy, sharpened our innovation, and strengthened our partnerships. We are proud to have met that test not by compromising our standards, but by raising them. At Kuangya, we believe that challenges are the crucible of leadership. We move into the future more confident than ever in our ability to engineer the reliable, high-performance electrical systems that will power the next phase of the global energy transition.